Back to School 2016

Spending expectations are high. We help you set a better budget!

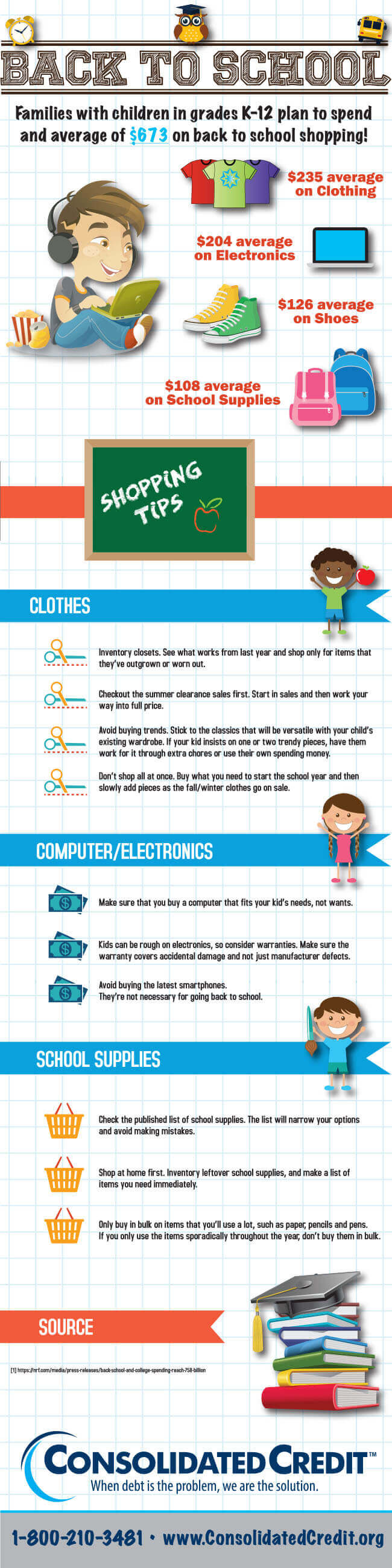

The back to school shopping season is the second most expensive time of year after the winter holidays for families and spending expectations this year are even higher than last year. The infographic shows where parents plan to spend along with tips to help you save.

More ways we help you save

In addition to this infographic, we have more ways we’re helping you save big on Back to School shopping this year. We’ll be hosting a Facebook Live on August 10 to talk about back to school budgeting and how to really save money this year.

Using credit strategically as you shop

The tips in the infographic are designed to help you cut back on your budget so you don’t spend as much. Hopefully that means you won’t have to rely on credit cards to cover your back to school costs – ideally you want to cover all of your back to school purchases with cash so you don’t add to your overall debt load.

However, that doesn’t mean you necessarily have to avoid credit cards when you shop. You may choose to use credit strategically during back to school shopping, particularly if you have a rewards credit card that offers incentives for you to use that card for back to school purchases. For example, the popular cash-back rewards credit card Chase Freedom offers 5% cash back during August and September on purchases made at wholesale clubs like Sam’s, BJ’s and Costco.

In this case, it may be beneficial to use that credit card to make your bulk school supply purchases. You just have to be strategic about how you use your credit cards and how you pay off the debt once it’s incurred.

Here’s how to maximize cash-back rewards without increasing your debt:

- Set up a back to school budget before you shop.

- Include all planned purchases from clothes and electronics to school supplies.

- Check your accounts to see if you have funds available to cover the total, using either free cash flow in your checking account or money from savings.

- If you don’t, review your back to school budget to make some cutbacks OR adjust your household budget to cut a few things you can do without this month.

- Ideally the rewards credit card you want to use should have a zero balance at the start of the billing cycle – this helps maximize cash back rewards by minimizing interest charges.

- Make your purchases, using your rewards credit card when it’s advantageous; otherwise, make purchases on debit or with cash.

- One you’ve finished shopping, use the money you have allocated in your checking or savings account to pay off the credit card balance in-full before the due date.

- Doing it this way will eliminate interest charges, so the cash back you earn isn’t offset by high APR interest charges.

If you can’t pay off the balance in full within one billing cycle or your rewards credit card already has a balance that you’re carrying over month to month, keep in mind that the rewards won’t be nearly as rewarding. After all, if you earn 5% cash back but it’s offset by interest charges on an 18% APR credit card that actually comes out to a net loss. So your reward credit cards are their most rewarding when you start and end every billing cycle with a zero balance. Paying off your balance in-full every month is how you make rewards truly rewarding.

Use this infographic

<a href="https://www.consolidatedcreditsolutions.org/infographics/back-school-2016/" target="_blank"><img src="https://www.consolidatedcreditsolutions.org/wp-content/uploads/2017/04/backtoschool_infographic-2016.jpg" alt="Graphic displaying tips on how to save money on school supplies" class="img-responsive" /></a>